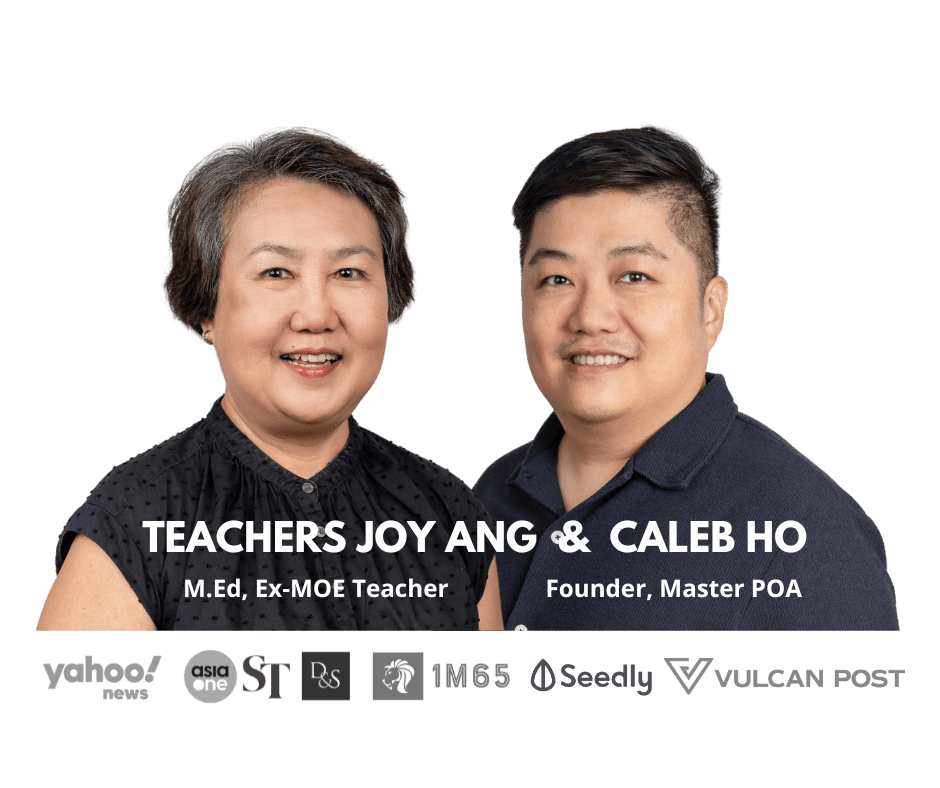

Jump Grades Education Presents

POA Tuition Singapore

Performance-targeted, student-centred POA tuition for G2/G3 O/N Level POA students

The Proven POA Tuition “LEAP”

Framework That’s Fun and Connects

Master Principles of Accounts tuition program provides a comprehensive curriculum based on the LEAP framework that is specifically designed for students struggling for the latest 7086/7087 GCE O/N Level Principles of Accounts syllabus by the Ministry of Education, Singapore.

Designed for struggling students

4.8

160+ Ratings

Over 8,000 POA students benefited from Master Principles of Accounts Study Guides and POA tuition classes since 2008.

Small Group Sizes

At Master Principles of Accounts, each skilled POA tutor works with students in a small group setting to foster a conducive learning environment during the tuition classes. Studying Principle of Accounts can be fun if there are right resources taught by engaging POA tuition teachers.

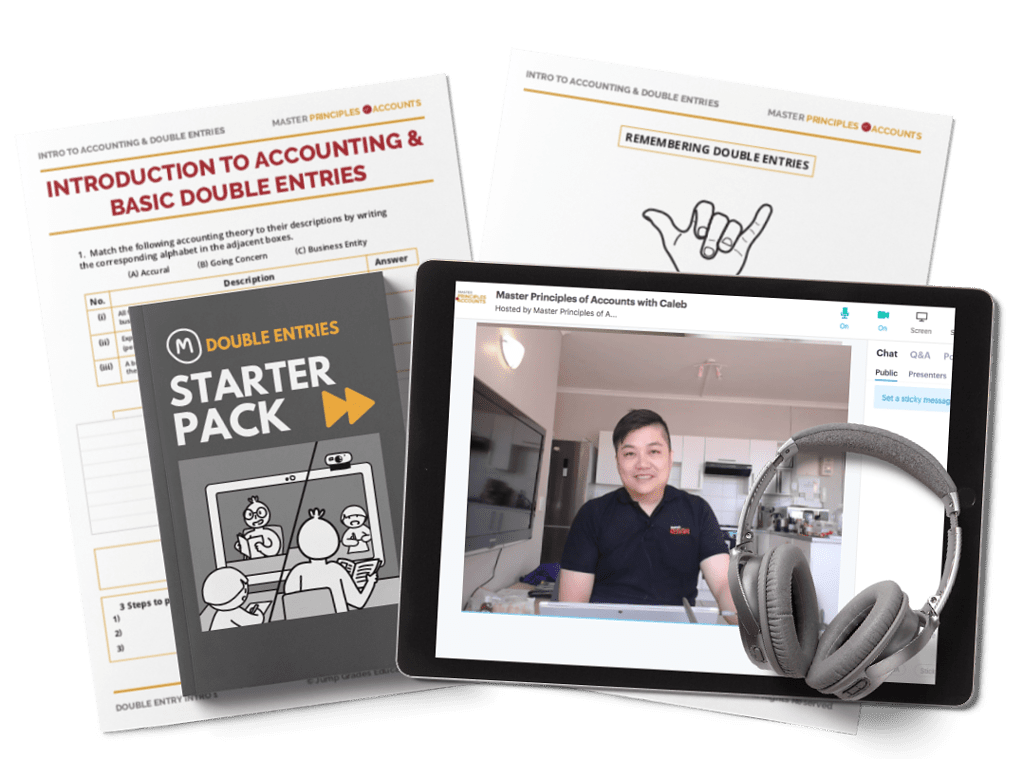

Student Learning Portal (Pocket Tutor)

Comprehensive online learning portal containing bite-size recorded lessons, step-by-step video explainers, quizzes and POA mock exam papers, complimentary to all our accounting POA tuition students

Get WA and mid year exam tips and hacks, exam techniques and in-depth coverage of heavy markers such as your balance day adjustments. All right in your pocket.

Looking for accounting POA tutors in Singapore?

2008

Year Founded

3000+

Students Taught

99+%

Pass Rate

POA FOUNDATIONS

BASICS CLASS

If you are totally new or unsure how you managed to pass your double entry basics ( or “I memorized”), the basics class is for you.

The Master POA Basics course is a two-lesson intensive class specifically designed for totally new or struggling students who need help with the basic double entries. Here, we build (or rebuild) your foundation before you join a regular POA tuition class for more advanced topics.

The Master POA Basics class is on a custom schedule and begins whenever there are 2-3 students who need help with the basics.

Testimonials

”

Caleb taught me easier methods to tackle different type of questions than what I learnt from school. With his guidance and consistent revision, I was able to jump to an A2 by O levels.

Anna Naveen

Bartley Secondary School

POA TUITION

WEEKLY SMALL GROUP POA TUITION

Small-classes are conducted throughout the week. The average class size of 8-12 is designed for maximum impact.

During our regular POA tuition class, students will apply the foundation debits and credits against the advanced topics. Using real life examples, the Master POA tutor breaks down the complex jargons and help students apply them in the POA exams.

Our regular, on-demand POA lessons will help you master the fundamentals of accounting and business reporting, as well as exam techniques to tackle and excel in your POA exams.

POA TUITION

WEEKLY 1:1 OR SMALL GROUP POA TUITION

Small-classes are conducted throughout the week. The average class size of 8-12 is designed for maximum impact.

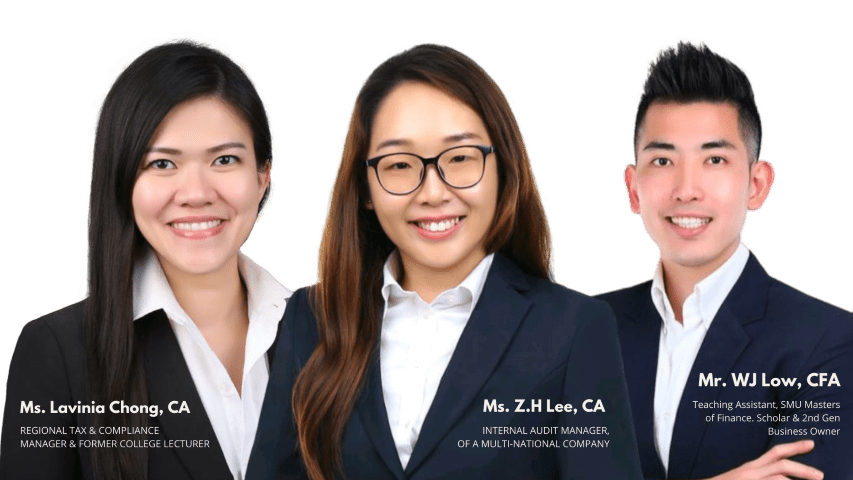

In Good Company

All Master POA students enjoy the same access to our curriculum delivered by qualified and handpicked tutors and trained with Master Principles of Accounts POA Tuition Curriculum.

Our tutors are practitioners, scholars and ex-MOE teacher. They are patient and relatable with decades of teaching experience. If you are an experienced POA tutor / accounting tutor in Singapore and love imparting your passion for POA, we would love to speak with you.

POA TUITION LEARNING MODES

1. Small Group Lessons

Weekly Classes (Onsite and Online)

Learn your way with onsite or online classes, both built on a proven teaching framework that drives results. Experience LIVE POA lessons that are interactive and structured to keep you accountable. Get individual marking and clear, actionable feedback after every lesson so you know exactly how to improve. Access past notes, worksheets, and lesson recordings anytime, and get help with your school homework so you never get stuck. Choose the format that fits your schedule and keep progressing with the same high standard of teaching and resources.

2. Online Portal

Master POA Online Course

Learn anytime, anywhere with bite-size 8 min-video lessons, quizzes with instant feedback and access the MPOA QnA forum with your MPOA peers and instructors. Review specific concepts over again if you get stuck.

Suitable for time-starved, motivated students who want to cover individual topics in-depth within a short time without committing to weekly POA tuition class.

Your Journey to Mastering POA Starts In Just

4 Simple Steps

Tell us about yourself

Let us know where you are at POA and if you need help with double entry basics plus your preferred learning mode.

Get expertly matched

Our program coordinator will pair you up with the perfect tutoring arrangement based on your profile and preference

Get your personalised study plan

Get a crystal clear roadmap to completing the syllabus in time for your exams – with specific timeline and topical coverage.

Embark on your learning journey

Get familiar with your tutor and experience what it is like to learn with Master Principles of Accounts

FREQUENTLY ASKED QUESTIONS

STOP STRUGGING & START THRIVING

ENQUIRE NOW

Call Me Back!

Fill up the form below. Our team will call you back within the next few business hours.